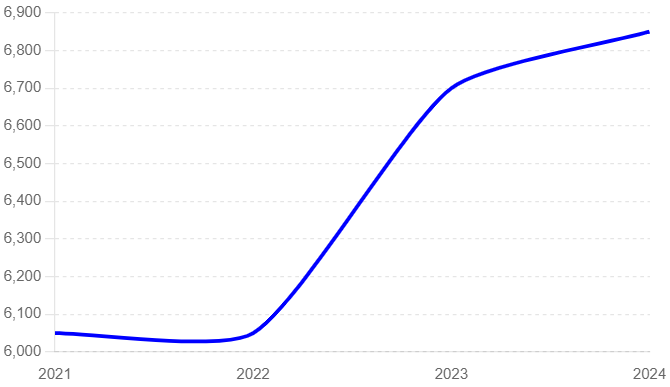

New shipbuilding price = Capesize bulker

Japanese shipowners, trading company shipping departments, and leasing companies are seeing a reduction in their fleet sizes. The primary reason is that operators have been exercising their purchase options (PO) since 2023. The number of ships affected by these PO exercises amounts to several dozen. Traditionally, shipowners have reinvested funds from POs and sales of used ships into new ship construction. However, with the soaring prices of new ships, they are currently unable to invest in new vessels as they had hoped.

“Three to four vessels have disappeared from our fleet due to the exercise of POs over the past year.”

A leasing company representative expressed this sentiment with a complex expression during an interview with the Japan Maritime Daily.

The leasing company in question primarily focuses on its Shipholding business. However, since last year, the secondhand ship market has been robust, leading operators to exercise their POs one after another. “We want to invest in new ships, but high ship prices and the difficulty of evaluating new fuels prevent us from doing so,” the representative stated.

A PO, or purchase option, refers to the right of an operator to choose whether to purchase or return a vessel owned by a shipowner, trading company shipping department, or leasing company upon reaching a certain charter period.

For operators, the decision to exercise a PO depends on whether the actual shipping and secondhand ship market conditions are more favorable at the time of the PO exercise compared to the start of the charter period. If market conditions are favorable, they purchase the vessel; if not, they return it to the shipowner. This right is considered unilaterally advantageous to operators, but the presence of a PO is usually determined by the contractual agreement between the operator and the shipowner at the time of signing the charter contract.

Some Japanese and overseas operators exercising POs are targeting bulk carriers and container ships completed between 2013 and 2014.

Following the Lehman Brothers collapse in September 2008, the market recovered between 2011 and 2012. Currently, many high-cost bulk carriers chartered by Japanese operators during that recovery period are subject to PO exercises. These vessels are mainly those reaching the 10-year contract mark.

The robust secondhand ship market from last year to this year has led multiple operators to exercise POs on ships they chartered during this period.

Taiwan’s Yang Ming Marine Transport announced through the Taiwan Stock Exchange this month that it would purchase three chartered container ships by exercising POs. The high demand for container ships, driven by the Suez Canal blockage, is a key factor behind this decision

The Danish shipping company Norden operates an average fleet of 367 bulk carriers and 100 product tankers, totaling 467 vessels. Of these, 82 charter contracts include POs.

Similarly, the Danish shipping company Ultrabulk has an average long-term charter period of six years. Considering Denmark’s tonnage tax system, they typically include POs.

Major Japanese shipowners who chartered Capesize vessels at high rates between 2011 and 2012 have reached the PO exercise period since last year. They purchased vessels during the PO period and, benefiting from the weak yen, sold them on the market.

The fleet sizes of shipowners, trading companies, and leasing companies whose vessels have been subject to PO exercises are shrinking.

Some trading company shipping departments aim to expand revenues through shipholding businesses. However, there is concern that ordering new ships at current high prices could result in significant latent losses in the future. “It is crucial to determine whether ordering new ships at the current (inflated) prices will lead to substantial latent losses in the future,” commented a shipping department representative.

In recent years, Japanese shipowners have become increasingly polarized between large and mid-sized or smaller companies. Large shipowners, backed by strong corporate credit, are ordering new ships, while mid-sized shipowners are hesitant to invest in new vessels.

Trading company shipping departments and leasing companies are struggling to generate profits through traditional brokerage businesses and are aiming to increase profits through Shipholding businesses. Both are unable to replenish their fleets, which have decreased due to POs.

Particularly, trading company shipping departments, which have recorded losses in the past with their Shipholding businesses alongside traditional brokerage, are cautious. “The current newbuilding prices are close to the highest levels compared to past prices,” noted a Tokyo-based trading company shipping department representative.

For trading company shipping departments within general trading companies to meet overall profit targets, “it is impossible to achieve this through brokerage business alone.”

Shipowners, trading company shipping departments, and leasing companies are facing difficult decisions on whether to invest to replenish their fleets lost through POs.

〆オペレーターがPOを行使しているため、日本船主や商社船舶部、リース会社の船隊規模が縮小している。

〆新造船価格が高騰しているため、彼らは新造船への投資に慎重になっており、船隊を補充できないでいる。

日本船主や商社船舶部、リース会社の保有船が減少している。2023年以降、オペレーター(運航船社)がパーチェスオプション(PO、船舶の購入選択権)を行使していることが主因である。POを行使された船舶は数十隻規模に上る。従来、船舶保有者はPOや中古船の売却資金を新造船に再投資してきた。現状は新造船価格の高騰で思うように資金を新造船に投資できない状況にある。